In December 2025, Nigeria's total public debt reached ₦159.28 trillion. Spread evenly across the country's 220 million people, that is roughly ₦724,000 per citizen, which is more than two months of median household income, charged to every man, woman and child between Sokoto and Bayelsa.

Most Nigerians do not feel this debt affects them directly. There is no envelope from the Debt Management Office, no quarterly bill, no court summons. The convenient fiction is that public debt is something the state owes, separate from the lives of those it governs.

This article argues the opposite. Public debt is the most efficient tax Nigeria has ever levied. It is collected silently through the price of fuel, the cost of an imported spare part, the interest on a working-capital loan, the rent on a one-bedroom flat in Yaba. It is paid by every household, every day, regardless of sector, age, or class. The four lives that follow show exactly how.

A government that owes ₦159 trillion has only one way to raise revenue

A state that has crossed Nigeria's threshold has three problems and one default response. The problems are that it cannot borrow at low rates, cannot raise taxes fast enough, and cannot grow its way out before the next election. The response is to push the cost onto households through monetary tightening, currency weakness, suppressed services, and forgone investment.

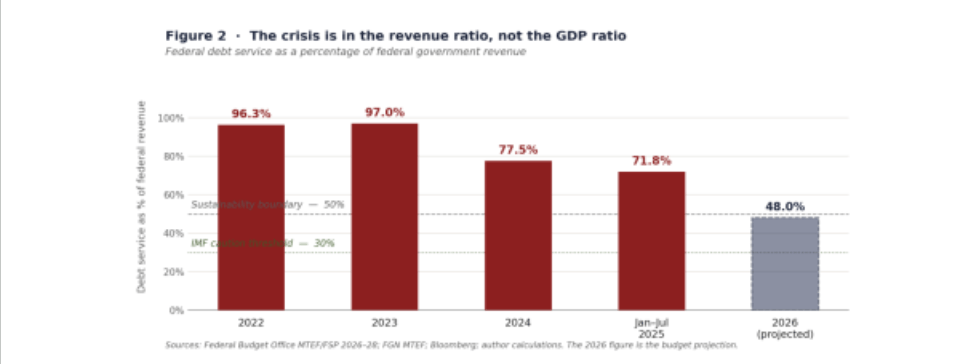

The transmission is not theoretical. The Central Bank's Monetary Policy Rate sits at 26.5 per cent following the MPC's May 2026 decision to hold, defending the naira against the consequences of fiscal indiscipline. Debt service alone consumed 71.8 per cent of aggregate federal revenue in the first seven months of 2025, and salaries plus debt service together exceeded total revenue — meaning the state borrowed merely to pay itself and its creditors. The 2026 budget projects debt servicing of about $11.6 billion, nearly half of projected government revenue, and only if the tax reforms deliver, which the first quarter shortfall of ₦2.24 trillion suggests they may not.

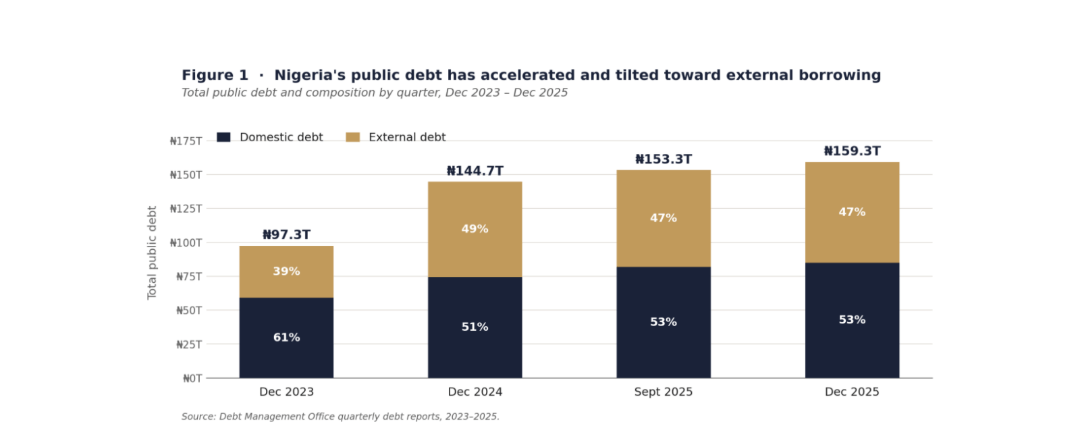

Two patterns are visible at once. The stock has risen by 64 per cent in two years from ₦97 trillion at the end of 2023 to ₦159 trillion at the close of 2025. Within that growth, the external share has crept up from 39 per cent to 47 per cent of the total, exposing more of the stock to currency risk and dollar-denominated interest costs at a time when the naira has fallen by nearly two-thirds against the dollar.

The ratio that matters is not the one most often cited. Debt-to-GDP, hovering around 36 per cent, sits well below the West African Monetary Zone ceiling of 70 per cent and looks comfortable in international comparisons. Debt-service-to-revenue tells a different story. Even at the improved 2025 reading of 71.8 per cent, the federal government devotes nearly three of every four naira it collects to creditors. The 2026 budget projects a fall to 48 per cent, still at the sustainability boundary, and only achievable if the tax reforms deliver, which the first-quarter shortfall suggests they will not.

These are not abstractions. They are the upstream conditions of four ordinary lives. Let’s take closer look

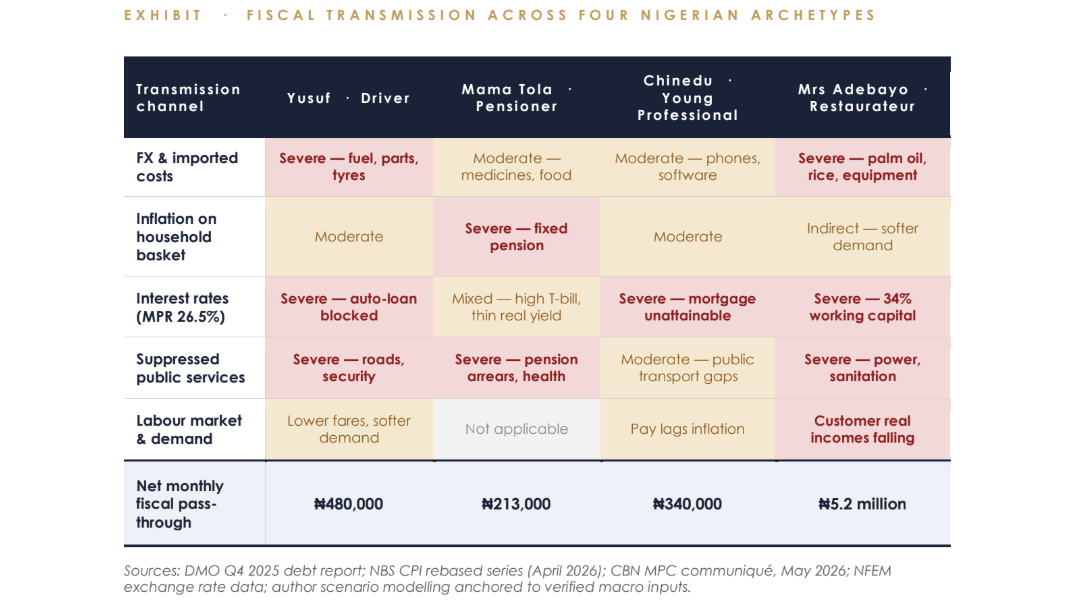

- Yusuf, 38, drives Bolt across the Lagos mainland

Yusuf runs a 2010 Toyota Corolla on the Bolt platform. He fills his tank twice a day to cover 200 kilometres across the mainland. In May 2023, premium motor spirit cost him ₦185 a litre. The same litre now costs roughly ₦950, a 414 per cent increase tied directly to the removal of the fuel subsidy that the federal government could no longer afford while servicing the debt it had accumulated to sustain it.

His arithmetic has changed completely. A 20-litre day cost him ₦3,700 in fuel before. It now costs him ₦19,000. To net the same ₦12,000 he used to take home daily, he must work an additional 3 hours, 6 days a week.

Three further squeezes compound the first. The naira-dollar rate of ₦1,371 per US dollar at the official window, down from ₦461 in mid-2023, has tripled the cost of imported spare parts and tyres — a brake-pad set that ran ₦18,000 in 2023 runs around ₦55,000 today. His insurance premium has risen accordingly. And the 26.5 per cent MPR means the auto

loan he was considering for a newer vehicle would carry a 32-36 per cent rate, putting a replacement car permanently out of reach.

“The debt did not knock on Yusuf's door. It came through his fuel tank.”

2. Mama Tola, 67, retired civil servant, Ibadan

Mama Tola retired from the Oyo State civil service in 2019. Her monthly pension is ₦142,000. In 2022, that pension bought her household roughly three weeks’ worth of essentials. The same basket today runs to about ₦355,000. Nigeria's official inflation rate of 15.69 per cent in April 2026 masks the fact that the rebased CPI started from a price level already 80 per cent higher than three years earlier.

The squeeze is structural, not cyclical. Her pension is a fixed-naira liability that federal and state governments must service alongside the debt — and when fiscal space collapses, pensioners are first in line for arrears. Her February stipend arrived in April. She is one of an estimated 35,000 retirees across multiple states whose payment cycles have been quietly stretched as governors triage between debt service, salaries, and statutory transfers.

She could move her ₦4 million in savings into 364-day Treasury bills yielding around 21 per cent — but that is the government borrowing from her at high rates to refinance debt her tax payments helped accrue. Even at 21 per cent, real returns after inflation are thin, and the rate is high precisely because the state's fiscal position is weak. The financial instrument designed to protect her has become the instrument of her continued capture.

The debt did not knock on Mama Tola's door. It came through her pension envelope, three months late.

3. Chinedu, 23, in his first year as a software engineer, Yaba

Chinedu earns ₦450,000 a month at a Lagos fintech. By the standards of his graduating class, he is doing well. The economics of doing well, however, have shifted under his feet.

His one-bedroom in Yaba costs ₦2.2 million annually, paid two years up front, a function of landlords pricing in inflation expectations and a Lagos housing market starved of mortgage finance, because mortgage rates anchored to the 26.5 per cent MPR sit at 28- 32 per cent. He pays ₦4.4 million for shelter before he buys his first plate of jollof.

His monthly arithmetic looks like this: ₦185,000 amortised rent and service charges; ₦95,000 transport and feeding; ₦55,000 data and utilities; ₦35,000 in family remittances. The residual, ₦80,000, is what his savings would be if they earned anything in real terms. They do not. Money-market funds yield 17-19 per cent. His real return, after official inflation of 15.7 per cent, is two to three percentage points, and that assumes the official figure reflects his actual consumption basket, which for a young urban professional it does not.

The country he begins his career in cannot offer him a mortgage, inflation-beating savings, or a job market valuing his skills in dollars without sending him abroad. Two of his three closest university friends now work in Toronto and Manchester. Nigeria's mid-skilled labour exodus is a result of public debt draining the fiscal space needed to build institutions that retain talent.

The debt did not knock on Chinedu's door. It came through his rent receipt and his friends' departure notices.

4. Mrs Adebayo, 44, owns a 32-cover restaurant in Wuse, Abuja

Mrs Adebayo opened her restaurant in 2019. In 2022, her net margin was 22 per cent. In Q1 2026, it was 9 per cent, and she has not raised menu prices to fully reflect input costs because her customer base- the same young professionals and civil servants whose real incomes have collapsed, would simply stop coming.

Her cost structure is a textbook in fiscal transmission. Diesel for her generator — six hours of grid power on a good day — costs ₦1.4 million monthly, up from ₦340,000 in 2022. Imported palm oil, rice and proteins move with the naira. Her working-capital line at the bank — ₦12 million — costs 34 per cent, which means she pays ₦4.1 million a year in interest alone. The Bank of Industry intervention fund she applied for has a six-month queue.

VAT, which the federal government raised to broaden the revenue base under fiscal pressure, takes 7.5 per cent off every plate. The newly empowered Nigeria Revenue Service has improved enforcement — which is good policy and necessary — but it is also expensive for a business whose margins have already collapsed.

Two of her staff left in 2025 and were not replaced. A third is on a reduced shift. She is, in net terms, deleveraging her own balance sheet by hollowing out her workforce — exactly what fiscally stressed economies do across the board, multiplied across thousands of small employers and tens of thousands of jobs.

The debt did not knock on Mrs Adebayo's door. It came through her diesel invoice, her bank statement, and her thinning staff list.

The same bill, in different envelopes

The transmission channels are stable across the four lives. What varies is the angle of impact.

Every citizen feels at least two channels. Most feel three. The combined effect is that the ₦159 trillion debt is not, in any meaningful sense, an external liability of the state. It is a distributed liability of the population, paid daily, in instalments calibrated to each person's exposure.

What follows

Three things are true at once.

First, Nigeria's debt-to-GDP ratio of around 34.7 to 39 per cent for 2026, depending on GDP rebasing, does not, by international convention, signal a crisis. The crisis is in the revenue ratio. When over 50 per cent of revenue goes to creditors, fiscal space collapses, and that is now Nigeria's structural condition.

Second, the household burden documented above is not a forecast. It is the present, already priced into Yusuf's daily fuel run, Mama Tola's pension lag, Chinedu's rent slip and Mrs Adebayo's diesel invoice. The transmission is complete.

Third, the political economy that produced ₦159 trillion of debt is intact. The same incentives to spend before elections, the same revenue weaknesses, the same patronage networks, the same wishful borrowing assumptions. Under the current administration, debt rose by roughly ₦66 trillion in just over two years, averaging about ₦29 trillion annually — compared with about ₦9.4 trillion per year on average under the previous government. The pace has accelerated. The architecture has not.

Three decisions sit before the next budget cycle. The first is whether new borrowing will be capped against verified tax-to-GDP rather than against an aspirational revenue base. The second is whether the Fiscal Responsibility Act will be amended to include enforceable subnational ceilings, given that 25 state governments have already breached their debt-to-IGR thresholds. The third is whether the contingent liabilities the current administration has incurred — including the ₦22.7 trillion in Ways and Means conversions, AMCON exposures, and state-government guarantees — will be fully disclosed before the 2027 transition.

If none of these decisions is taken, the bill in Yusuf's pocket, Mama Tola's pension envelope, Chinedu's rent receipt and Mrs Adebayo's diesel invoice will not get smaller. It will only get itemised.

The Centre for Inclusive Social Development (CISD) is a non-profit research and advocacy organisation working to advance inclusive governance, gender and social equity, civic technology, and sustainable livelihoods across Nigeria and sub-Saharan Africa. Through rigorous research, coalition-building, and public-interest storytelling, CISD amplifies the voices of marginalised communities and holds power accountable.

Learn more at cisdnigeria.org or follow us on social media.

How to cite this article

Folahan Johnson. (2026, June 1). The bill is already in your pocket: Why ₦159 trillion in public debt is the most efficient tax Nigeria has ever levied — and how it arrives, daily, in four ordinary lives.. CISD Insights. Centre for Inclusive Social Development. Retrieved from https://cisdnigeria.org/article/the-bill-is-already-in-your-pocket/.